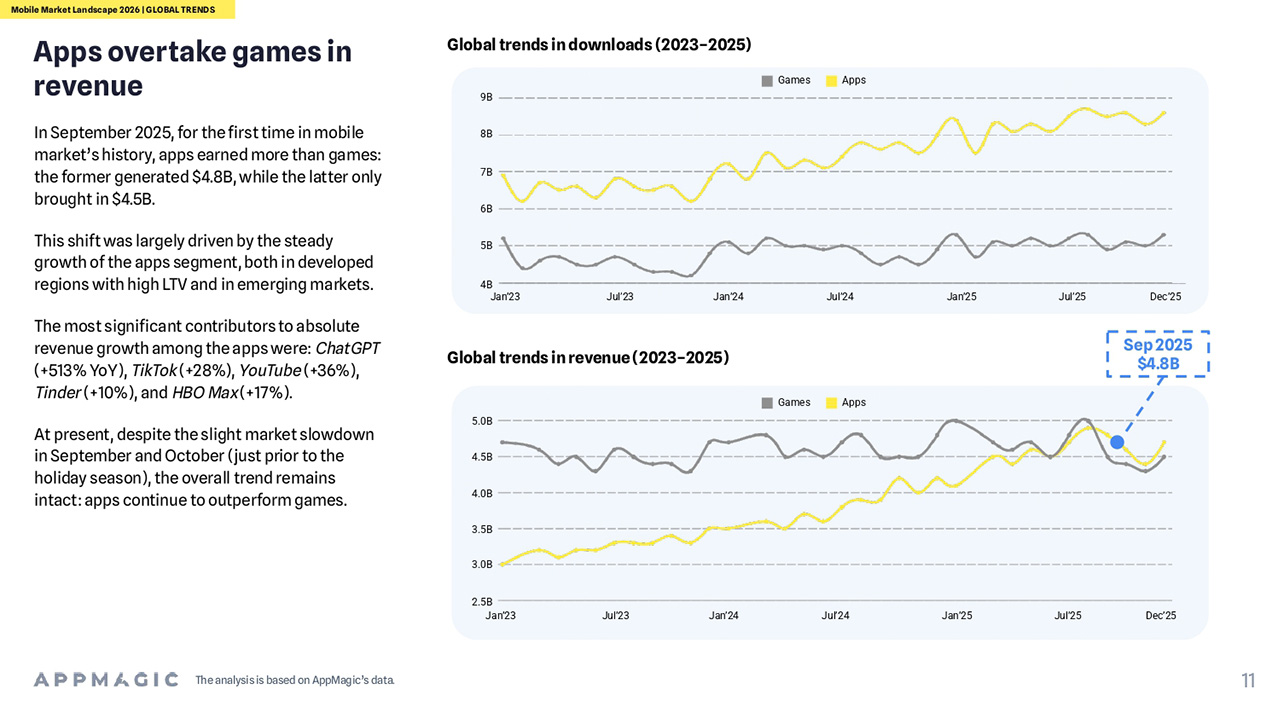

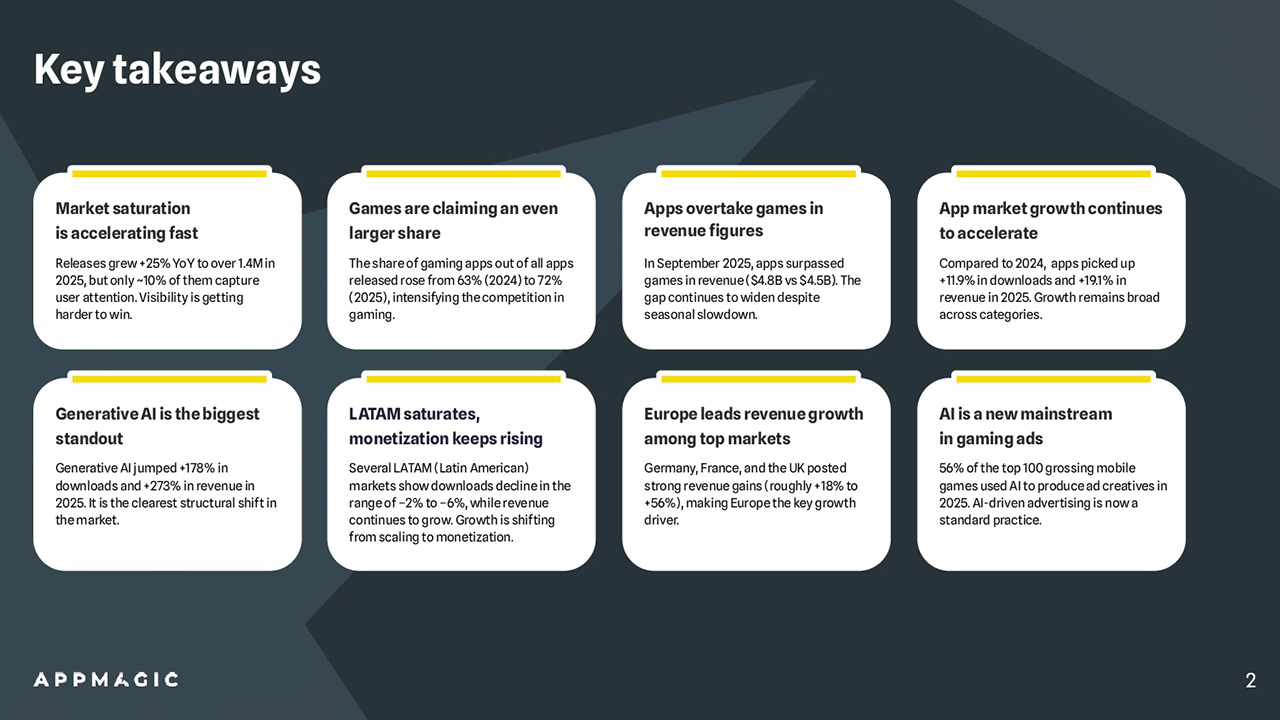

According to the latest Mobile Market Patterns Report, 2026, published by AppMagic, there was a major shift in the mobile application market in 2025: for the first time, income from non-play applications went beyond game applications, while artificial intelligence became an industry-wide standard tool. Applied markets: historical inverse of non-play income and increased competition The month of September 2025 was a historic turning point, with an income of $4.8 billion for one-month non-play applications, up from $4.5 billion for games. Despite the seasonal slowdown, the gap continues to widen, marking significant changes in mobile ecosystems. The overall application market was strong in 2025, with downloads increasing by 11.9 per cent compared to 2024, income by 19.1 per cent and growth being widespread rather than concentrated in only a few areas. User attention to the new heights reached in 2025: applications increased by 25 per cent per year to over 1.4 million, but only about 10 per cent of them received meaningful user participation. The share of game applications in total distribution also increased from 63 per cent in 2024 to 72 per cent in 2025.

Generating AI applications grew most alarmingly, with a 178 per cent increase in downloads and a 273 per cent surge in income in 2025, one of the clearest structural changes in mobile markets. ChatGPT led this round of expansion, with income of $2.33 billion, an increase of 51 per cent over the same period. Google Gemini was also used on a large scale, with a 381 per cent increase in downloads.

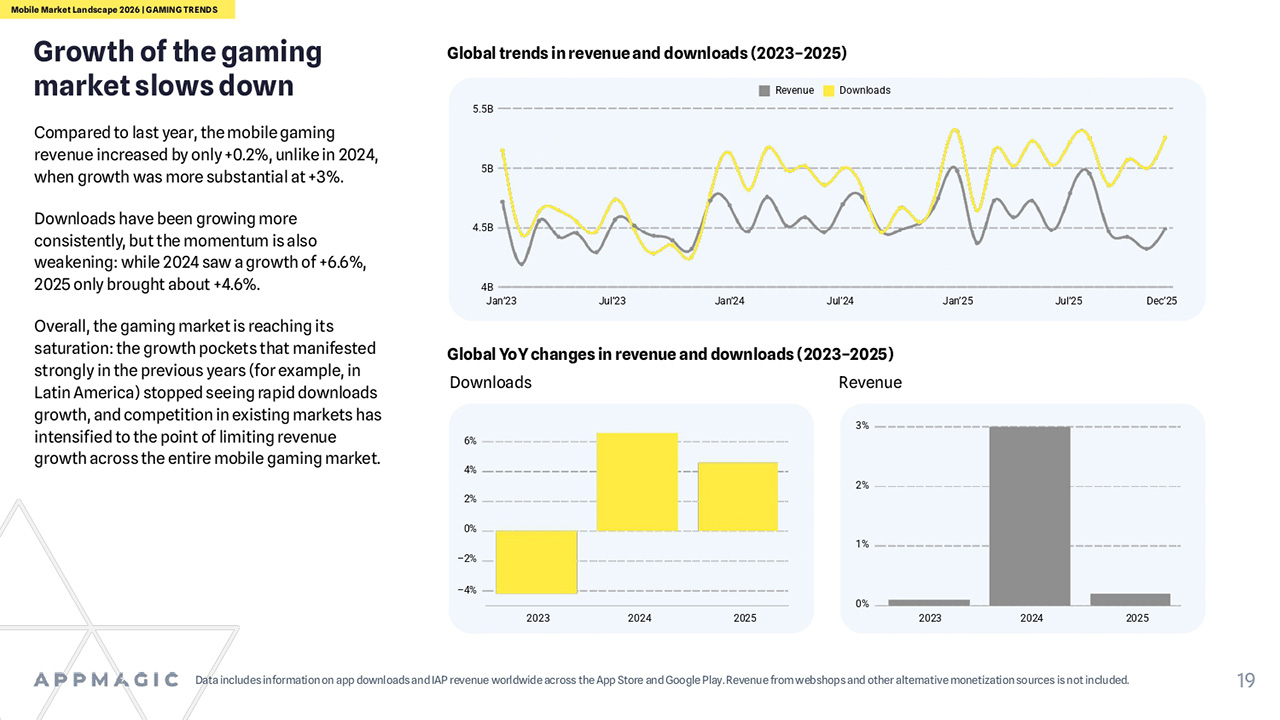

Artificial intelligence has become standard practice in the marketing of mobile games: a hand-show analysis of the top-income 100 shows that 56 of AI’s advertising materials were used in 2025, marking that AI-driven advertising has become a norm rather than a test. Game markets: slowing growth, strategic leadership, increasing D2C trend Growth in the field of games slowed, with income increasing by only 0.2 per cent (compared with 3 per cent in 2024) and downloads by 4.6 per cent (down from 6.6 per cent in the previous year). The strategic-type games performed well, with a 16 per cent increase in input and a 15 per cent increase in downloads. However, there has been a decline in RPG and casino-like games, of which casino-type game income has fallen by 7.6 per cent, although downloads have increased by 15.8 per cent, suggesting that income sources are shifting to channels outside traditional applied shops.

Face-to-face consumer (D2C) liquidity mode is favoured in games. The D2C income in the United States market increased by 26 per cent over the same period, while the D2C earnings from the top 100 games increased by 38 per cent. Europe has become a key growth driver, with growth ranging from 18 to 56 per cent in Germany, France and the United Kingdom. Latin American markets showed signs of saturation, with multi-country downloads falling by 2 to 6 per cent, but income continued to grow, indicating that developers were more focused on current users rather than expanding their audience. In major markets, Indonesia registered a 10 per cent increase in downloads, while India and the United States remained stable.

Trends in other categories of application In addition to generating AI, there are significant trends in several application categories: Entertainment type:Steady growth was maintained, with income increasing by 17.6 per cent and downloads increasing by 11 per cent. Short play applications led to expansion, with downloads increasing by 280 per cent and income by 94 per cent. Tool class:The focus shifted from user acquisition to realization, with a 20.6 per cent jump in income and a 7.2 per cent increase in downloads. Cloud storage remains the most important source of income for this category. Social categories:Downloads stagnated (0.1 per cent), but income increased by 8.6 per cent. Dating applications continue to be the largest source of income, while the real-time communications and blog-based applications have grown more strongly, from 23 to 30 per cent.

Related Posts